(Mises Institute)—French philosopher Auguste Comte (1798-1857) is purported to have said that, “Demography is destiny,” meaning that a country’s future is determined by the size and age distribution of its population. The concept also helps explain how individuals within a given generation fare throughout their lives.

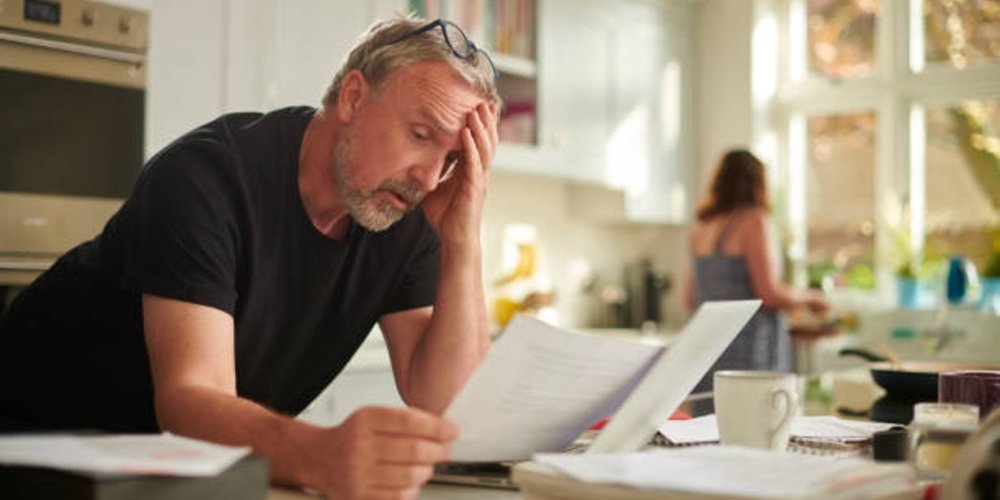

America’s Generation X includes those born from 1965 through 1980, now aged 45-60. They number 65 million individuals, representing 19.5 percent of the entire US population, somewhat fewer than those in the older Baby Boomers at 20.9 percent, or the younger Millennials at 21.7 percent. They are now entering leadership roles in public and private sectors of the economy, and are often caring for both their children and their own aging parents. Some are sending their children to college at historically-inflated tuition levels for what is increasingly questionable indoctrination rather than genuine education. The oldest of the group are in their peak earning years, contemplating their retirement in a few short years, while the youngest may be just becoming aware of the importance of retirement planning.

A Shift in Pension Plans

The transition from defined-benefit pension plans to defined-contribution 401(k) plans occurred during Gen X’s working years, uniquely affecting the generation’s retirement planning. Both types of pension plans typically deduct employee contributions from paychecks, sometimes matched by employers, but the similarity ends there.

Traditional defined-benefit plans entrust these retirement monies to employer pension managers who invest the funds to generate sufficient funding to pay the promised pensions. Thus employers bear the risks associated with investing the retirement funds. Defined-contribution plans, on the other hand, allow employees to self-direct their retirement funds, usually within employer-approved investment options. These plans place investment risk on employees. Most Gen X individuals entered the labor market during the economy-wide transition from defined-benefit pension plans to defined-contribution 401(k) accounts.

Some defined-benefit plans, especially in the public sector, are struggling with sizable unfunded liabilities, meaning that the plans have promised more pension benefits than they have in reserves to pay these benefits. This means that employers—that is, taxpayers in the case of public sector retirement plans—will have to cover the shortfall in order to pay the promised benefits. Courts have typically found defined-benefit plans to be contractual obligations that cannot be altered if employers have unfunded liabilities.

Gen X’s experience demonstrates that significant changes in employer practices and federal law can affect the wherewithal of an entire generation of Americans. The two primary laws that affect 401(k) plans are the Employee Retirement Income Security Act (ERISA) and the Setting Every Community Up for Retirement Enhancement (SECURE) Act. ERISA—passed in 1974—outlines the rights of consumers whose assets are invested in retirement accounts, including 401(k) accounts. The SECURE Act—passed in 2019—is intended to encourage retirement savings and provides annual increases in employees’ tax-free contributions to 401(k) accounts.

As a generation so directly impacted by the transition from one retirement paradigm to another, Gen X-ers missed out on some of the automatic features in the early days of 401(k) plans, such as automatic enrollment at time of employment and annual increases in deferred contribution limits.

Recent Surveys of Gen X Reveal Conflicting Results

It is not entirely clear how prepared for retirement Gen X-ers may be. On the one hand, the 2024 Annual Retirement Study from Allianz Life Insurance Company of North America reveals some disconcerting results on Gen X’s retirement saving and on retirement itself:

- Many of the Gen X-ers surveyed say that they can’t afford to retire at 65; and a quarter of those without a 401(k) account don’t expect to ever retire at all

- 44 percent say they currently have a plan for how they will take income in retirement

- 48 percent worry they will be forced to live too frugally and not enjoy retirement as much

- 45 percent worry about how to best take distributions from their retirement savings for income during retirement

- 35% worry that they will outlive their retirement plan assets

- Nearly half have done no retirement planning

- They predict they will need an average $1,069,746 in savings in order to retire comfortably, yet they expect to have just $602,944 saved by then

On a more positive note, the Bank of America Institute has found that, although Gen X discretionary spending has been weak compared to that of other generations, Gen X-ers are saving more as they age. Interestingly, Gen X’s investments per household are now 40 percent higher than those of the overall population.

Social Security: The Elephant in the Room

In addition to their employment pensions and other retirement savings, Gen X-ers hope to receive some Social Security benefits—as those in previous generations have and future generations should anticipate having. Yet—with the projected insolvency of the Social Security Trust Fund and resulting reductions in benefits within ten years if Congress fails to act—the retirement survey findings summarized above are disconcerting. While Social Security was never designed to provide all of America’s retirement needs, it has for nine decades provided a backstop to prevent poverty among retired seniors.

Social Security is best viewed as an intergenerational redistribution of income from younger working Americans to older retired Americans, accomplished with a 6.2 percent payroll tax levied on all earned income up to an annual wage-base limit, $176,100 in 2025. Employers are similarly assessed at 6.2 percent of their employees’ earned income. Those who are self-employed must pay both their own 6.2 percent payroll tax and the 6.2 percent employer tax, a total of 12.4 percent, since they are effectively their own employers.

Payroll tax revenues go into the Social Security trust fund, where they are then directly disbursed as benefits to eligible retired individuals. For this reason, some have cynically described Social Security as a Ponzi scheme, in which the later contributors (younger working generations) are taxed to pay for benefits paid to earlier contributors (older Americans receiving benefits).

Misconceptions about Social Security

Social Security was never designed to be a pension plan, yet employees contribute to the program during their working years as they might to a proper pension plan. Employees could probably have accumulated more retirement funds through a defined-contribution plan than with a mandatory Social Security payroll tax, but the program has historically conveyed to the nation an appealing aura of shared social welfare.

After his re-election in 2004, George W. Bush announced his support of individually-managed accounts within Social Security, similar to 401(k) accounts, but the public response to individual accounts was so negative that he never pursued it in his second term, nor have subsequent presidents followed up on the notion.

Paying the payroll tax is a necessary, but not sufficient, condition to receive Social Security benefits. A 1960 Supreme Court decision in Fleming v. Nestor clarified that Social Security was meant to be a form of long-term social insurance, not a contractual government benefit, therefore, merely having contributed payroll tax does not entitle an individual to benefits. It had been—and still is among many Americans—a common misconception that paying the tax is sufficient to receive benefits, but the 1960 decision still governs, and the Court has never revisited the matter.

Gen X and Social Security

If Congress takes no action, the projected insolvency of the Social Security trust fund will affect Gen X. The oldest of the generation—born in 1965, currently age 60—will be eligible to apply for benefits at age 62 in 2027. The youngest Gen X-ers will not be able to apply until 2042. Benefits for all generations could be reduced by about 25 percent, imposing hardship on many seniors.

Elected officials remain mum on plans to assure Social Security’s future viability. The 2024 presidential candidates vowed not to cut benefits, yet offered no plans such as increasing the benefit eligibility age, revising benefit calculations, or increasing the payroll tax, measures most recently taken by the Reagan administration in 1983 to assure Social Security’s future. One can make an educated guess that—rather than overseeing a 25 percent benefit reduction—most politicians would opt to fund benefits from general tax revenues if the trust fund is inadequate. This would require Congressional action.

Once again, comparable to the transition from defined-benefit pension plans to defined-contribution 401(k) plans, Gen X will likely be affected by political action to assure the future of Social Security. Such is the fate of Gen X-ers as the old adage that “demography is destiny” impacts their lives in real time.

It’s becoming increasingly clear that fiat currencies across the globe, including the U.S. Dollar, are under attack. Paper money is losing its value, translating into insane inflation and less value in our life’s savings.

Genesis Gold Group believes physical precious metals are an amazing option for those seeking to move their wealth or retirement to higher ground. Whether Central Bank Digital Currencies replace current fiat currencies or not, precious metals are poised to retain or even increase in value. This is why central banks and mega-asset managers like BlackRock are moving much of their holdings to precious metals.

As a Christian company, Genesis Gold Group has maintained a perfect 5 out of 5 rating with the Better Business Bureau. Their faith-driven values allow them to help Americans protect their life’s savings without the gimmicks used by most precious metals companies. Reach out to them today to see how they can streamline the rollover or transfer of your current and previous retirement accounts.

Kamala Harris Says the American Dream Is “Gone”

by Modernity News

During a pre recorded interview, Kamala Harris once again failed to deliver any substantive outline of her policies, primarily attacking Donald Trump’s outlook and his first term in office. At one point when speaking about the economy, Harris appeared to suggest, in stark contrast to Trump, that the American Dream…

Gold Price Forecasts Skyrocket Following Moves by China and the Fed

by Sponsored Post

With the Federal Reserve beginning what most expect to be a sustained easing cycle, momentum continues to rise for gold and silver. Values have been steadily rising and the newest forecasts point to even more gains down the road. At the end of September, BMO Capital Markets published updated commodity…

Taxes and Tariffs and Trade: Oh My! Trump’s Plan to Bolster the Economy

by Just The News

In a bid to build a broader coalition, former President Donald Trump has outlined a vision of tax cuts, import tariffs, and “reciprocal trade” to preserve and restore American industries. Since coming down the escalator of Trump Tower in 2015, the Republican standard bearer has espoused unconventional trade policies and…

Expert Testimony: Mass Immigration Under Biden-Harris Is Driving Up Rents for Americans

by Breitbart

The arrival of millions of foreign nationals, many of whom are illegal aliens, under President Joe Biden and Vice President Kamala Harris is helping to drive up rents for working- and middle-class Americans, an expert witness told Congress Wednesday. Center for Immigration Studies Director of Research Steven Camarota told the…

This Year Marks First Since 1958 That Us Held No Oil and Gas Lease Sales

by Just The News

This year will be the first year since 1958 that the Bureau of Ocean Energy Management held no offshore oil and gas lease sales. Energy expert Alex Epstein, author of “Fossil Future,” argued at a recent House Budget Committee hearing the United States’ record-high oil production is in spite of…

Kamala’s Devastating Middle Class Taxes

by Independent Sentinel

With the election coming up, the IRS plans to reduce our taxes for 2025. it’s a common tactic to make it seem like they won’t tax us into oblivion once they return to office. CBS News: Some Americans could see lower federal income taxes in 2025 due to an annual…

Congress Passes Stop-Gap Spending Bill After Failed Mike Johnson Gambit

by Breitbart

Congress on Wednesday passed legislation that would fund the government through nearly the end of December. The House and the Senate passed a stop-gap spending bill that would push the government spending deadline to December 20. The measure, otherwise known as a continuing resolution (CR), keeps federal spending the same….

A ‘Bipartisan’ Bar Tried to Open in DC, Then Libs Cried That an Elephant Image Was ‘Hurtful.’

by The National Pulse

A new bar in Washington, D.C., whose political theme focused on bipartisan agreement and debate, succumbed to partisan pressure before the establishment could even serve its first drink. Originally billed as Political Pattie’s, the bar was flooded with complaints by liberals who said the establishment’s logo—specifically the Republican Elephant—was offensive…

Newsom Signs Bill Requiring Janitors to Take $200 Sexual Harassment Training

by Just The News

California Gov. Gavin Newsom signed a bill requiring companies that hire janitors to make sure janitors take sexual assault training every other year, and pay $200 per participant for sessions with under 10 janitors present, and $8 for sessions with 10 or more janitors. The bill also requires the government…

Biden-Harris Regime Prepares Another $8 Billion in Military Aid for Ukraine During Zelensky’s Washington Visit

by The Gateway Pundit

The Biden-Harris regime is once again prioritizing foreign interests over the well-being of American citizens, with plans to announce an eye-watering $8 billion in military aid for Ukraine during Ukrainian President Volodymyr Zelensky’s visit to Washington. This massive giveaway comes as Americans continue to face economic hardships, skyrocketing inflation, and…

‘Economic Dystopia:’ Silicon Valley Tycoon Predicts AI Will Take Over 80% of All Work

by Breitbart

Vinod Khosla, legendary Silicon Valley investor and entrepreneur, has predicted that AI will replace the majority of work in most jobs, necessitating the implementation of universal basic income (UBI) to prevent economic instability and inequity. Fortune reports that in a recent blog post, Vinod Khosla, the billionaire co-founder of Sun…